Ever filled a prescription for a generic drug and been shocked by the price? You’re not alone. Many people assume insurance means lower costs-but for generics, that’s not always true. Sometimes, paying cash is cheaper than using your insurance. Why? It all comes down to how insurers, pharmacies, and middlemen called Pharmacy Benefit Managers (PBMs) negotiate prices behind the scenes. This isn’t a simple system. It’s layered, confusing, and often works against the patient.

Who’s really setting the price?

The price of a generic drug isn’t set by the manufacturer, the pharmacy, or even your insurer directly. It’s decided by PBMs-companies that act as middlemen between drug makers, insurers, and pharmacies. Think of them as contractors hired to cut costs. But instead of lowering prices for you, they often create hidden layers of profit. The three biggest PBMs-OptumRx, CVS Caremark, and Express Scripts-control about 80% of the market. That means they have enormous power over what drugs you can get and how much you pay.

Here’s how it works: PBMs negotiate with drug companies to get discounts based on how many pills they promise to move. In return, drug makers lower their list prices. But here’s the catch: those list prices are still used to calculate your copay. So even though the drug cost less to produce, your insurance plan might still charge you based on the original high price. Meanwhile, the PBM pockets the difference.

How the pricing formula hides the real cost

Pharmacies get reimbursed for filling prescriptions using a formula that’s anything but transparent. Most commonly, they’re paid based on either the National Average Drug Acquisition Cost (NADAC) or the Average Wholesale Price (AWP), plus a small dispensing fee. But here’s where things get strange.

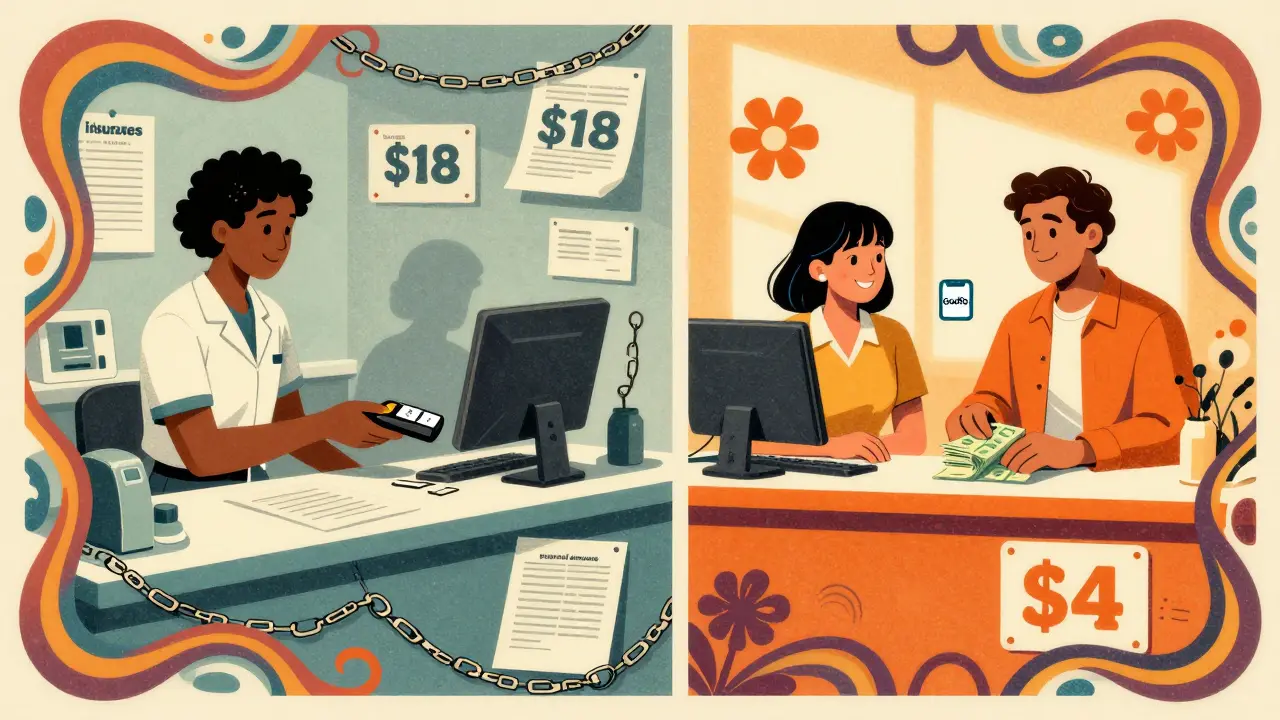

PBMs charge your insurance plan one price for the drug, then pay the pharmacy a lower amount. The difference? That’s called spread pricing. It’s not a fee. It’s profit-and it’s hidden. For example, your plan might be billed $45 for a generic blood pressure pill, but the pharmacy only gets $12 back. You pay $15 as your copay. The PBM keeps $18. You never see it. And if you paid cash at the pharmacy, you might have paid only $4.

This isn’t rare. A 2024 Consumer Reports survey found that 42% of insured adults had paid more out-of-pocket for a generic drug than the cash price. One Reddit user reported paying $45 through insurance for a drug that cost $4 cash. Another said their $50 generic diabetes pill cost $7 cash. These aren’t outliers. They’re symptoms of a broken system.

Why your insurance doesn’t always save you money

You’d think having insurance means lower prices. But for generics, the system often works the opposite way. PBMs design formularies-lists of approved drugs-to steer patients toward ones that give them the biggest rebates. That doesn’t always mean the cheapest drug. It means the drug that gives the PBM the highest kickback from the manufacturer.

So your plan might cover a $12 pill but not a $7 one-even if the $7 pill works just as well. Why? Because the manufacturer of the $12 pill gave the PBM a bigger rebate. The PBM makes more money, even if you pay more. And because of gag clauses in contracts, pharmacists aren’t allowed to tell you that paying cash would be cheaper. That’s legal in most states.

Even when you think you’re getting a deal, you’re not. A 2023 Wall Street Journal investigation found that some cancer and multiple sclerosis generics cost insured patients more than double what cash payers paid. The same drug, same pharmacy, same day. The only difference? Whether you used insurance.

What happens at the pharmacy counter

Pharmacists are stuck in the middle. They have to run your prescription through multiple PBM systems, each with different rules. Some use NADAC. Others use AWP. Some add fees. Others subtract them. One pharmacy owner told me they spend over 250 hours a year just trying to understand what each PBM will pay. That’s more than six full workweeks-just to figure out how much they’ll get reimbursed.

And it gets worse. PBMs sometimes do “clawbacks.” That’s when they approve a claim, pay the pharmacy, then later demand money back because they changed their mind about the reimbursement rate. Sixty-three percent of independent pharmacies have experienced this. Many can’t afford to fight it. Between 2018 and 2023, over 11,000 independent pharmacies shut down because they couldn’t survive the low, unpredictable reimbursements.

Smaller pharmacies also have to run two pricing systems: one for insurance, one for cash. That means double the software, double the training, double the mistakes. Setup costs for the right billing software? Around $12,500 per pharmacy. Most can’t afford it. So they rely on the big chains-which are owned by PBMs. That’s how the same company that sets your price also owns the pharmacy you go to.

Who wins? Who loses?

Let’s break it down:

- Drug makers win by getting rebates based on volume. They can keep raising list prices because the PBM gets more money the higher the price goes. That’s why list prices for some generics have doubled in five years-even though production costs haven’t changed.

- PBMs win big. They made $15.2 billion in 2024 from spread pricing alone, and 68% of that came from generic drugs. That’s pure profit from hidden markups.

- Insurers win by keeping premiums low. They don’t want to raise your monthly bill, so they shift costs to your copay and deductible. That’s why your premiums haven’t gone up much, but your out-of-pocket costs have.

- Patients lose. We’re paying more, getting less transparency, and being kept in the dark.

And here’s the kicker: generics make up 90% of all prescriptions but only 23% of total drug spending. That means we’re using generics to save money-but the system is designed to make us pay more, not less.

Change is coming-slowly

There are signs the system is cracking. In September 2024, the Biden administration ordered PBMs to stop spread pricing in federal programs like Medicare and Medicaid. That rule takes effect in January 2026. States are also stepping in. As of late 2024, 42 states have passed or are considering laws to force PBMs to disclose their pricing practices.

The Medicare Drug Price Negotiation Program, started under the Inflation Reduction Act, is now negotiating prices for 20 drugs. Experts estimate it could save $200-250 billion over ten years-if it expands to private insurance. And legislation like the Pharmacy Benefit Manager Transparency Act of 2025 would require PBMs to pass 100% of rebates to insurers, cutting out the hidden profit.

But the pharmaceutical industry says this system is necessary to fund innovation. That’s true-sort of. The money saved from eliminating spread pricing wouldn’t go to drug makers. It would go to patients and insurers. The real question is: why should PBMs profit from your confusion?

What you can do right now

You don’t have to wait for policy changes to protect yourself.

- Always ask the pharmacist: "What’s the cash price?" Even if you have insurance, it might be cheaper.

- Use apps like GoodRx or Cost Plus Drugs. They show real-time cash prices and often beat insurance copays.

- If your copay is higher than the cash price, file a complaint with your insurer. Demand an explanation.

- Ask if your employer offers a transparent plan. Only 12% do-but they exist.

- When possible, choose 90-day supplies. They often have lower per-pill costs and fewer billing errors.

Generic drugs are supposed to be affordable. They’re not. The system isn’t broken-it was built this way. But you don’t have to accept it.

Why is my insurance copay higher than the cash price for a generic drug?

Because your insurer and the Pharmacy Benefit Manager (PBM) negotiated a price that includes hidden markups. The PBM charges your plan one amount, pays the pharmacy less, and keeps the difference-called spread pricing. Meanwhile, your copay is based on the inflated list price, not the real cost. Paying cash often bypasses this system entirely, so you pay the true wholesale price.

Do PBMs always make drugs more expensive for patients?

Not always-but they often do. PBMs are designed to maximize profit for themselves and their parent companies, not to minimize patient costs. When they steer patients toward drugs with higher rebates (not lower prices), patients end up paying more. In many cases, especially with generics, the cash price is significantly lower than the insured price.

What is spread pricing and how does it affect me?

Spread pricing is when a PBM charges your insurance plan one price for a drug, then pays the pharmacy a lower price for filling it. The difference is kept by the PBM as profit. You never see this. But if your copay is based on the higher price your plan was charged, you end up paying more than the drug actually costs. This is why your $15 copay might be higher than the $4 cash price.

Can pharmacists tell me if cash is cheaper?

In most states, no-because of "gag clauses" in PBM contracts. These clauses legally prevent pharmacists from telling you the cash price is lower than your insurance copay. That’s why you need to ask. Some states have banned these clauses, but enforcement is uneven. Always check the cash price yourself.

Are there any alternatives to using my insurance for generics?

Yes. Apps like GoodRx, SingleCare, and Cost Plus Drugs let you compare cash prices across pharmacies and often offer coupons that bring prices down to $5 or less for common generics. Some employers offer direct primary care or pharmacy discount programs. And if you have a Health Savings Account (HSA), you can use pre-tax dollars to pay cash prices-sometimes saving 70% or more.